March Electronic Components Sales Sentiment Slips in March, Misses Expectations

ATLANTA - The most recent results of ECIA’s ECST survey show sales sentiment slipping slightly from the recent highs it hit in February. In the February survey participants had anticipated improving sales sentiment in March.

However, the actual results for March show overall sentiment falling by 2 points down to 88.6.

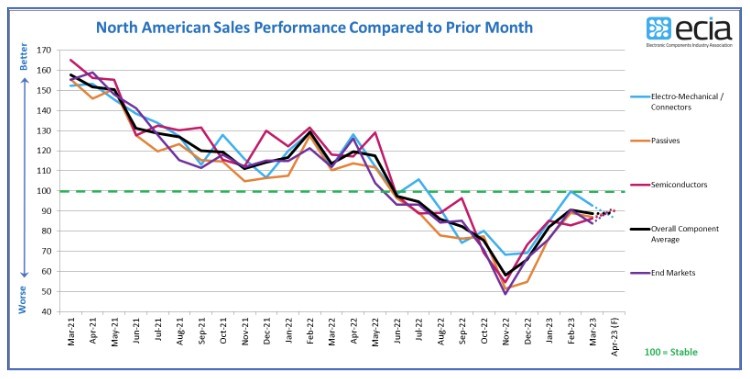

“The index score had been improving consistently from its low in November with encouraging increases in December, January, and February,” explained ECIA Chief Analyst Dale Ford. “During this time the overall index improved by 32.6 points and hit 90.6 in February, the best reading since July 2022. In this context, a dip of 2 points is fairly minor. Any index result below 100 indicates sentiment declining on month-to-month sales. The good news is that the sentiment stabilizes at this level with a small increase to 89.1 for the April outlook. Overall, the most recent electronic component sentiment measures indicate ongoing sales declines. However, these results would still point to a “soft landing” in this current cycle,” he said.

While the Electro-Mechanical Components sentiment index achieved the highest level again in March, it slipped substantially from the February high of 99.9 to 92.7 in March. The outlook for this segment is increasingly pessimistic as the April outlook drops to 86.7 which would be the lowest score among the three component categories in April. On the other hand, Semiconductors saw improved results in March as the measure grew from 82.9 to 86.3. This improving index score carries into the April outlook with expectations of a score of 90.0. The index results for Passive Components steer a middle course for the three categories as it dips by 2.1 points in March then rebounds in the April outlook to 90.5. Overall, the most recent electronic component sentiment measures indicate ongoing sales declines. However, these results would still point to a “soft landing” in this current cycle. The end-market results in the March survey follow the same trend as the component results with the overall index dipping by 4.2 points. There were stark contrasts among the individual market segments.

The highest scoring segments all slipped in their results with Medical Electronics dropping below 100. Avionics/Military/Space, Automotive, and Industrial were able to sustain scores at 100+. The most positive news in the end-market results was the strong rebound among the three lowest scoring markets: Computer, Consumer and Telecom Mobile Phones. These segments saw their scores jump between 9.2 to 16.1 index points. Telecom networks comes in lowest among all markets at 74.6.

The best news in the most recent survey is found in the results for product lead time trends. Overall lead time sentiment showed declining lead time sentiment improve from 37% to 43% and the combined stable to declining lead times improve from 90% to 96%. There is very little evidence of increasing lead time pressure with only 2% of participants seeing increasing lead times in Semiconductors. The weak market demand is clearly the primary contributor to the major improvement in the lead time picture. However, some credit does need to be given to increased production. Given the overall assessment that inventory overhang is the greatest challenge facing the supply chain currently, product mix issues would appear to be the main contributor to any reports of increasing lead times as inventories balance out in the declining market.

PCB East, the electronics industry trade show for the East Coast

May 9-12, 2023

Press Releases

- Green Circuits Names Adam Szychowski Chief Revenue Officer

- MicroCare Appoints Doug Kay as Director of Market and New Business Development

- Altus Group Expands Soldering Portfolio with SEHO Partnership

- Seika Machinery to Kick Off SMI 2026 Webinar Series with Focus on Solder Paste Preparation and Control